Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, December 16, 2010

How to Get Rich Slowly DRIP by DRIP: Transaction History

Instructions for the transaction history a Computershare DRIP stock are provided in the slide show below. But it works best if your browser is Internet Explorer. The slide show is narrated, but only if you download it into PowerPoint.

Friday, December 10, 2010

How to Get Rich Slowly DRIP by DRIP - Set Up a One-Time Investment

Instructions for setting up a Computershare DRIP stock for a one-time investment are provided in the slide show below. The slide show is narrated, but only if you download the it into PowerPoint.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, December 2, 2010

How to Get Rich Slowly DRIP by DRIP: Setting Up for Dividend Reinvestment

Instructions for setting up a Computershare DRIP stock for automatic dividend reinvestment are provided in the slide show below. The slide show is narrated, but only if you download the it into PowerPoint.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, November 25, 2010

How to Get Rich Slowly DRIP by DRIP: Gifts to My Children

Motivation

My kids are both adults. They live in Texas and I live in Virginia. I talk to them on the phone occasionally but seldom see them.

During the first few years of being half a continent away I still thought I knew them pretty well; enough that I could pick birthday and Christmas gifts for them that they’d like.

But, as the years went by they grew older - less & less like the teenagers I remembered. Buying presents became difficult.

During this same time my interest & knowledge about investing grew. And along the way I discovered DRIP accounts.

Discovery

After experimenting with my own DRIP for about a year I thought of opening DRIP accounts in the names of my two adult children. The idea was to take money I would normally spend for their Christmas and birthday presents and use it to buy shares of stock. I could also use the DRIP accounts and occasional statements to teach them about compound interest, dollar-cost averaging, and dividends; and, to encourage them to begin investing in their own future.

Preparation

The first thing I did was to prepare Excel spreadsheets that demonstrated the power of compound interest. The spreadsheets also demonstrated the affect of various monthly investment amounts over a range of years and growth rates.

A key to making the whole thing work was getting their consent and commitment to making no attempt at withdrawing money from the accounts and allowing me to managing them.

In the end, I selected a stock, Hasbro (HAS), and added that stock to my own DRIP account. Then I filled out transfer forms for each of my kids. Next, I visited them in Texas and explained the Excel spreadsheets, DRIP accounts, and my plan to buy stock with their birthday & Christmas money.

Having secured their commitments to not mess with the accounts until after my death, they signed the transfer forms.

I mailed the transfer forms to Computershare, the Hasbro transfer agent. A few weeks later I received confirmation from Computershare that one share of HAS stock had been successfully transferred to each of the kid’s DRIP accounts.

Finally, I set up accounts in the kid’s names on the Computershare web site.

Execution

The accounts were now set up. My plan was ready to execute. I took the remainder of my birthday & Christmas budget and spread it out over the following year in $25 dollar increments; dollar-cost averaging into Hasbro stock.

Twice a year, May & December, I send the kids an activity statement showing the investments made and the current account value.

During the second year I added another stock and in the third year I added a third stock. The total annual investments remain the same. I just allocate the investments to different stocks at different times. I don’t have an automatic monthly investment set up. I manually prepare each one and use an Outlook task reminder to schedule investments and to keep me on budget.

The next time I visit them in Texas, I plan to review those Excel spreadsheets with them again - including the actual results from their DRIP accounts. I hope to encourage them to start putting a little of their own money into the DRIP or into their own Roth IRA account.

In the next post I’ll take a close look at administering a DRIP account after the initial set up.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

My kids are both adults. They live in Texas and I live in Virginia. I talk to them on the phone occasionally but seldom see them.

During the first few years of being half a continent away I still thought I knew them pretty well; enough that I could pick birthday and Christmas gifts for them that they’d like.

But, as the years went by they grew older - less & less like the teenagers I remembered. Buying presents became difficult.

During this same time my interest & knowledge about investing grew. And along the way I discovered DRIP accounts.

Discovery

After experimenting with my own DRIP for about a year I thought of opening DRIP accounts in the names of my two adult children. The idea was to take money I would normally spend for their Christmas and birthday presents and use it to buy shares of stock. I could also use the DRIP accounts and occasional statements to teach them about compound interest, dollar-cost averaging, and dividends; and, to encourage them to begin investing in their own future.

Preparation

The first thing I did was to prepare Excel spreadsheets that demonstrated the power of compound interest. The spreadsheets also demonstrated the affect of various monthly investment amounts over a range of years and growth rates.

A key to making the whole thing work was getting their consent and commitment to making no attempt at withdrawing money from the accounts and allowing me to managing them.

In the end, I selected a stock, Hasbro (HAS), and added that stock to my own DRIP account. Then I filled out transfer forms for each of my kids. Next, I visited them in Texas and explained the Excel spreadsheets, DRIP accounts, and my plan to buy stock with their birthday & Christmas money.

Having secured their commitments to not mess with the accounts until after my death, they signed the transfer forms.

I mailed the transfer forms to Computershare, the Hasbro transfer agent. A few weeks later I received confirmation from Computershare that one share of HAS stock had been successfully transferred to each of the kid’s DRIP accounts.

Finally, I set up accounts in the kid’s names on the Computershare web site.

Execution

The accounts were now set up. My plan was ready to execute. I took the remainder of my birthday & Christmas budget and spread it out over the following year in $25 dollar increments; dollar-cost averaging into Hasbro stock.

Twice a year, May & December, I send the kids an activity statement showing the investments made and the current account value.

During the second year I added another stock and in the third year I added a third stock. The total annual investments remain the same. I just allocate the investments to different stocks at different times. I don’t have an automatic monthly investment set up. I manually prepare each one and use an Outlook task reminder to schedule investments and to keep me on budget.

The next time I visit them in Texas, I plan to review those Excel spreadsheets with them again - including the actual results from their DRIP accounts. I hope to encourage them to start putting a little of their own money into the DRIP or into their own Roth IRA account.

In the next post I’ll take a close look at administering a DRIP account after the initial set up.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, November 18, 2010

How to Get Rich Slowly DRIP by DRIP: Gifts to Children

For your own investments you have many choices besides DRIP accounts. Starting with an employer-sponsored 401k plan and including Traditional and Roth IRA accounts available from just about every financial institution of any type. Even life insurance and annuity contracts are investment options.

However, for your grandson or your niece your choices are limited. The amount of money you can afford to invest for them is also likely more limited. The limitations make DRIP accounts an attractive choice.

With a series of one-time investments of $25.00 in any month you can invest annual amounts ranging from $25.00 to $300.00. Of course, you can invest significantly more than $300.00 a year. But the more money you can commit to the child’s investment the more investment choices you have.

DRIP’s are perfect for the grandparent of modest means. With low periodic contributions completely under your control, you can make a huge difference in a child’s financial outcome.

Accounts for minor children can be set up as “custodial” accounts. For adult children they can be set up in the name of the adult child and, with the cooperation of the adult child, managed by you – the contributor.

In the next post I’ll review the DRIP accounts I set up for my adult children.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

However, for your grandson or your niece your choices are limited. The amount of money you can afford to invest for them is also likely more limited. The limitations make DRIP accounts an attractive choice.

With a series of one-time investments of $25.00 in any month you can invest annual amounts ranging from $25.00 to $300.00. Of course, you can invest significantly more than $300.00 a year. But the more money you can commit to the child’s investment the more investment choices you have.

DRIP’s are perfect for the grandparent of modest means. With low periodic contributions completely under your control, you can make a huge difference in a child’s financial outcome.

Accounts for minor children can be set up as “custodial” accounts. For adult children they can be set up in the name of the adult child and, with the cooperation of the adult child, managed by you – the contributor.

In the next post I’ll review the DRIP accounts I set up for my adult children.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Wednesday, November 10, 2010

How to Get Rich Slowly DRIP by DRIP: Asset Allocation

Asset Allocation and rebalancing are disciplines that force you to “buy low and sell high” without trying to time the market. For them to work you must be invested in two or more uncorrelated products (investment vehicles) – preferably negatively correlated (meaning that when one goes up the other goes down).

The Limits of DRIP Asset Allocation

DRIP investments are essentially limited to large-cap dividend-paying stocks, with a few international ADR’s and a few mid-cap stocks thrown in for flavor. Because of this limitation, diversification of asset classes is a matter of selecting dividend-paying stocks from different industries and countries.

My Diversification Plan

Currently, my DRIP portfolio contains:

1. HAS (Hasbro) – an American toy company

2. SJM (J M Smucker) – an American food company

3. CTL (CenturyLink) – an American telephone company

4. JNJ (Johnson & Johnson) – an American pharmaceutical & medical equipment company

I’m also planning to add:

5. BHP (BHP Billiton) an Australian mining company.

6. A suitable non-US oil & gas company.

My portfolio is reasonably diversified across industry sectors. However, it could be improved by the addition of an industrial like Nucor (NUC), a defense company like General Dynamics (GD), a utility like NextEra Energy (NEE), and a financial like Cincinnati Financial (CINF).

The Main Weakness of My Portfolio

My portfolio’s main weakness is its concentration in American stocks. This is an historical accident. As I learned more, I added to the portfolio. Plus, my primary Transfer Agent, Computershare, sponsors few international choices. BHP Billiton is offered thru Wells Fargo Shareholder Services. It’ll be my 1st foray into alternative DRIP Transfer Agents.

If I eventually add more companies to the planned 6-stock portfolio, I’ll focus on international companies. However, there’re some US based companies, like Coke (KO) that receive more than 70% of their revenue from outside of North America. I’d count them as international even if they’re headquartered in the US.

Assign Asset Allocation Percentages

Once a DRIP portfolio has been acquired, or perhaps chosen in advance, it’s time to decide what portion of the portfolio will be targeted for each stock and ADR. A simple even distribution works just fine. For example, if you have a five-stock DRIP portfolio you might assign a target of 20% of the total market value to each of the five stocks.

There’re no rules for this percentage allocation. It depends entirely on how you feel about the relative risk and return of each investment. You may consider your utility stock to be the safest investment and chose to allocate a higher percentage of the portfolio value to it. And, you might decide that your integrated oil company stock is certain to appreciate as oil supplies become more expensive world-wide. If so, your asset allocations might be 35% in the utility, 35% in the integrated oil and 10% in each of the other three stocks.

Again, there’re no rules except the ones you make. However, once made, change the rules seldom or the benefit of rebalancing will be lost.

Portfolio Rebalancing

Selling DRIP stocks is much harder and more expensive than buying them. That’s good. It encourages you to choose carefully, buy consistently, and hold your stocks for a long time. However, it also limits your flexibility in rebalancing your DRIP portfolio.

Your primary method of rebalancing is to allocate new money to stocks that are below their target values leaving those above their targets alone. This makes rebalancing take longer – spreading it out over a number of months of continuous investment.

Most financial advisors recommend rebalancing a portfolio every year. Some recommend every other year. Others advise watching the portfolio every month but rebalancing only when it gets out of balance by more than 15% or 20%.

The differences in advice are largely due to different approaches to getting the most benefit from the “buy low & sell high” discipline. Letting a “hot” investment run far enough to capture a significant gain before taking the gain is always a tradeoff with the timing of when the “hot” investment will cool.

Market timing being something few people can pull off consistently, you must establish a rule for when you’ll rebalance. Once established, this rule must be adhered to and seldom changed. Or, once again, you’ll lose the benefit of the rebalancing discipline and be no more successful at timing the market than the rest of humanity.

To Sum Up

1. Select a diversified portfolio of DRIP stocks & ADR’s based on industry and country.

2. For each stock choose a target allocation (a percentage of the portfolio value) and change the targets reluctantly.

3. Decide when, or under what conditions, you’ll rebalance your DRIP portfolio back to the target allocation percentages.

4. Execute the rebalancing as planned by redirecting your new monthly investments until the target allocations are restored.

The next topic will be using DRIP’s as gifts to children – or grandchildren.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

The Limits of DRIP Asset Allocation

DRIP investments are essentially limited to large-cap dividend-paying stocks, with a few international ADR’s and a few mid-cap stocks thrown in for flavor. Because of this limitation, diversification of asset classes is a matter of selecting dividend-paying stocks from different industries and countries.

My Diversification Plan

Currently, my DRIP portfolio contains:

1. HAS (Hasbro) – an American toy company

2. SJM (J M Smucker) – an American food company

3. CTL (CenturyLink) – an American telephone company

4. JNJ (Johnson & Johnson) – an American pharmaceutical & medical equipment company

I’m also planning to add:

5. BHP (BHP Billiton) an Australian mining company.

6. A suitable non-US oil & gas company.

My portfolio is reasonably diversified across industry sectors. However, it could be improved by the addition of an industrial like Nucor (NUC), a defense company like General Dynamics (GD), a utility like NextEra Energy (NEE), and a financial like Cincinnati Financial (CINF).

The Main Weakness of My Portfolio

My portfolio’s main weakness is its concentration in American stocks. This is an historical accident. As I learned more, I added to the portfolio. Plus, my primary Transfer Agent, Computershare, sponsors few international choices. BHP Billiton is offered thru Wells Fargo Shareholder Services. It’ll be my 1st foray into alternative DRIP Transfer Agents.

If I eventually add more companies to the planned 6-stock portfolio, I’ll focus on international companies. However, there’re some US based companies, like Coke (KO) that receive more than 70% of their revenue from outside of North America. I’d count them as international even if they’re headquartered in the US.

Assign Asset Allocation Percentages

Once a DRIP portfolio has been acquired, or perhaps chosen in advance, it’s time to decide what portion of the portfolio will be targeted for each stock and ADR. A simple even distribution works just fine. For example, if you have a five-stock DRIP portfolio you might assign a target of 20% of the total market value to each of the five stocks.

There’re no rules for this percentage allocation. It depends entirely on how you feel about the relative risk and return of each investment. You may consider your utility stock to be the safest investment and chose to allocate a higher percentage of the portfolio value to it. And, you might decide that your integrated oil company stock is certain to appreciate as oil supplies become more expensive world-wide. If so, your asset allocations might be 35% in the utility, 35% in the integrated oil and 10% in each of the other three stocks.

Again, there’re no rules except the ones you make. However, once made, change the rules seldom or the benefit of rebalancing will be lost.

Portfolio Rebalancing

Selling DRIP stocks is much harder and more expensive than buying them. That’s good. It encourages you to choose carefully, buy consistently, and hold your stocks for a long time. However, it also limits your flexibility in rebalancing your DRIP portfolio.

Your primary method of rebalancing is to allocate new money to stocks that are below their target values leaving those above their targets alone. This makes rebalancing take longer – spreading it out over a number of months of continuous investment.

Most financial advisors recommend rebalancing a portfolio every year. Some recommend every other year. Others advise watching the portfolio every month but rebalancing only when it gets out of balance by more than 15% or 20%.

The differences in advice are largely due to different approaches to getting the most benefit from the “buy low & sell high” discipline. Letting a “hot” investment run far enough to capture a significant gain before taking the gain is always a tradeoff with the timing of when the “hot” investment will cool.

Market timing being something few people can pull off consistently, you must establish a rule for when you’ll rebalance. Once established, this rule must be adhered to and seldom changed. Or, once again, you’ll lose the benefit of the rebalancing discipline and be no more successful at timing the market than the rest of humanity.

To Sum Up

1. Select a diversified portfolio of DRIP stocks & ADR’s based on industry and country.

2. For each stock choose a target allocation (a percentage of the portfolio value) and change the targets reluctantly.

3. Decide when, or under what conditions, you’ll rebalance your DRIP portfolio back to the target allocation percentages.

4. Execute the rebalancing as planned by redirecting your new monthly investments until the target allocations are restored.

The next topic will be using DRIP’s as gifts to children – or grandchildren.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, November 4, 2010

How to Get Rich Slowly DRIP by DRIP: Diversification in a DRIP

Purposes

The purpose of a DRIP (Dividend ReInvestment Plan) is:

1. To growth your net worth with a combination of capital appreciation and reinvested dividends.

2. To supplement your income with a dividend stream that increases faster than inflation.

3. To do these things with minimum transaction costs.

The purpose of diversification is to reduce the risk to your net worth of a failure of any one investment or of a secular decline in any one asset class.

Limits of Diversification

These purposes restrict your investment choices to dividend-paying common stocks and ADR’s (American Depository Receipts). In practice, you’re also restricted to “large-cap” stocks; companies with a total market capitalization of more than $10 Billion. Market capitalization means the market value of all of the shares held by all shareholders.

Unfortunately, few mid-cap and small-cap stocks support DRIP’s.

In addition, I’m restricting myself to DRIP’s with minimum follow up investments of $50 per transaction or less; with a strong preference for $25 or less.

Consequently, the opportunity to diversify your DRIP holdings is limited. You can, however, choose to set up DRIP’s with companies in different industry sectors and from different countries.

My Diversification Plan

Currently, my DRIP portfolio contains:

1. HAS (Hasbro) – an American toy company

2. SJM (J M Smucker) – an American food company

3. CTL (CenturyLink) – an American telephone company

4. JNJ (Johnson & Johnson) – an American pharmaceutical & medical equipment company

I’m also planning to add:

5. BHP (BHP Billiton) an Australian mining company.

6. A suitable non-US oil & gas company.

Ideal Portfolio Size

I think a DRIP portfolio of from 5 to 10 stocks is ideal. More than that would be cumbersome – you’d be better off using a brokerage account.

Less than 5 is okay – especially at first. But, I think your intention should be to diversify over time. It really doesn’t require more money to diversify your DRIP portfolio. You just have to allocate where your monthly investment money goes. For example, if you have only $25 per month to invest, you can invest in a different stock each month or each quarter or each year. You’ll end up with fewer shares of each stock but with the same investment stream you can have a five stock portfolio instead of just one.

Speaking of allocating your investments – the next post will cover Asset Allocation in your DRIP portfolio.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

The purpose of a DRIP (Dividend ReInvestment Plan) is:

1. To growth your net worth with a combination of capital appreciation and reinvested dividends.

2. To supplement your income with a dividend stream that increases faster than inflation.

3. To do these things with minimum transaction costs.

The purpose of diversification is to reduce the risk to your net worth of a failure of any one investment or of a secular decline in any one asset class.

Limits of Diversification

These purposes restrict your investment choices to dividend-paying common stocks and ADR’s (American Depository Receipts). In practice, you’re also restricted to “large-cap” stocks; companies with a total market capitalization of more than $10 Billion. Market capitalization means the market value of all of the shares held by all shareholders.

Unfortunately, few mid-cap and small-cap stocks support DRIP’s.

In addition, I’m restricting myself to DRIP’s with minimum follow up investments of $50 per transaction or less; with a strong preference for $25 or less.

Consequently, the opportunity to diversify your DRIP holdings is limited. You can, however, choose to set up DRIP’s with companies in different industry sectors and from different countries.

My Diversification Plan

Currently, my DRIP portfolio contains:

1. HAS (Hasbro) – an American toy company

2. SJM (J M Smucker) – an American food company

3. CTL (CenturyLink) – an American telephone company

4. JNJ (Johnson & Johnson) – an American pharmaceutical & medical equipment company

I’m also planning to add:

5. BHP (BHP Billiton) an Australian mining company.

6. A suitable non-US oil & gas company.

Ideal Portfolio Size

I think a DRIP portfolio of from 5 to 10 stocks is ideal. More than that would be cumbersome – you’d be better off using a brokerage account.

Less than 5 is okay – especially at first. But, I think your intention should be to diversify over time. It really doesn’t require more money to diversify your DRIP portfolio. You just have to allocate where your monthly investment money goes. For example, if you have only $25 per month to invest, you can invest in a different stock each month or each quarter or each year. You’ll end up with fewer shares of each stock but with the same investment stream you can have a five stock portfolio instead of just one.

Speaking of allocating your investments – the next post will cover Asset Allocation in your DRIP portfolio.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Friday, October 29, 2010

How to Get Rich Slowly DRIP by DRIP: What's Dollar-Cost Averaging Got to do with It?

Dollar-Cost Averaging is a fancy term for a series of regular equal value investments into the same product over an extended time regardless of the product’s changing price.

Generally, people make equal periodic investment purchases for their own convenience; they match their buys with their employer’s payroll cycle. People with 401k plans, including me, are almost always dollar-cost averaging into their 401k investments for example.

So what? Who cares?

Virtually no one can successfully time the market over a long period. You can’t always correctly predict the price of your chosen investment in order to buy when it’s low and sell when it’s high.

Since you really don’t know which way the market will go in the near term, if you make a single lump-sum investment you may accidentally buy just before the price goes up. You may also buy just before the price crashes.

One reason to Dollar-Cost Average is to reduce the price direction risk of a fixed dollar investment. Spread your $10,000 lump-sum investment as 10 monthly investments of $1,000 each and you'll find the entry prices of each of the 10 investments are different. Some are higher and some lower than the first purchase.

The hope is that your average price is better than your single lump-sum price would've been.

Happiness is a Volatile Share Price

But, there’s another advantage of long term Dollar-Cost Averaging – the kind available thru monthly DRIP account purchases. The Excel workbook below shows the number of shares that would be purchased and their value if equal annual investments were made in a DRIP over 25 years with all dividends reinvested. It also assumes that the DRIP stock increases in value at a consistent 6% rate every year.

6% Constant Annual Earnings Per Share Growth

After 25 years of $600 annual investments the investment grows to $63,563.21 with 448.54 shares in the account at a presumed market price of $141.71 per share. The sum of the annual investments is only $14,994.05 – a pretty good return overall.

The next Excel workbook shows an example of what happens in reality. The stock price doesn’t grow steadily every year. Instead it bounces around. Sometimes up. Sometimes down. But, in the end, it reaches the same price - $141.71 per share.

6% Average EPS Growth with Volatility

The difference is each annual $600 investment buys either more shares or less as the share price fluctuates.

The example has 6% average annual growth but with fluctuations of 18.12% up or down around the average. The result is an ending value of $77,916.60 with a total of 549.83 shares in the account.

Try it for Yourself

Obviously, I forced the ending share price to be the same by tweaking the fluctuation percentage. You can change the parameters in the workbook to see how different values of average growth or the volatility (fluctuation percentage) affect the outcome. But the typical case is that volatility, as long as some of it takes the price below the average increase curve, will result in more shares held in the end.

That’s why Warren Buffet says to be happy when share prices fall – Mr. Market is just holding a sale!

The next post will take up the idea of “diversification” in DRIP accounts.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Generally, people make equal periodic investment purchases for their own convenience; they match their buys with their employer’s payroll cycle. People with 401k plans, including me, are almost always dollar-cost averaging into their 401k investments for example.

So what? Who cares?

Virtually no one can successfully time the market over a long period. You can’t always correctly predict the price of your chosen investment in order to buy when it’s low and sell when it’s high.

Since you really don’t know which way the market will go in the near term, if you make a single lump-sum investment you may accidentally buy just before the price goes up. You may also buy just before the price crashes.

One reason to Dollar-Cost Average is to reduce the price direction risk of a fixed dollar investment. Spread your $10,000 lump-sum investment as 10 monthly investments of $1,000 each and you'll find the entry prices of each of the 10 investments are different. Some are higher and some lower than the first purchase.

The hope is that your average price is better than your single lump-sum price would've been.

Happiness is a Volatile Share Price

But, there’s another advantage of long term Dollar-Cost Averaging – the kind available thru monthly DRIP account purchases. The Excel workbook below shows the number of shares that would be purchased and their value if equal annual investments were made in a DRIP over 25 years with all dividends reinvested. It also assumes that the DRIP stock increases in value at a consistent 6% rate every year.

6% Constant Annual Earnings Per Share Growth

After 25 years of $600 annual investments the investment grows to $63,563.21 with 448.54 shares in the account at a presumed market price of $141.71 per share. The sum of the annual investments is only $14,994.05 – a pretty good return overall.

The next Excel workbook shows an example of what happens in reality. The stock price doesn’t grow steadily every year. Instead it bounces around. Sometimes up. Sometimes down. But, in the end, it reaches the same price - $141.71 per share.

6% Average EPS Growth with Volatility

The difference is each annual $600 investment buys either more shares or less as the share price fluctuates.

The example has 6% average annual growth but with fluctuations of 18.12% up or down around the average. The result is an ending value of $77,916.60 with a total of 549.83 shares in the account.

Try it for Yourself

Obviously, I forced the ending share price to be the same by tweaking the fluctuation percentage. You can change the parameters in the workbook to see how different values of average growth or the volatility (fluctuation percentage) affect the outcome. But the typical case is that volatility, as long as some of it takes the price below the average increase curve, will result in more shares held in the end.

That’s why Warren Buffet says to be happy when share prices fall – Mr. Market is just holding a sale!

The next post will take up the idea of “diversification” in DRIP accounts.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, October 21, 2010

How to Get Rich Slowly DRIP by DRIP: Transaction Costs Compared to Mutual Funds

You pay less for the privilege of investing in a DRIP account compared to mutual funds. Paying less means more of your money works for you - increasing your net worth.

The transaction costs for HAS (Hasbro), a typical DRIP stock, were discussed in the previous post. Hasbro’s fee schedule is reproduced below.

Example Fee Schedule

The fee structure for Hasbro (HAS) is:

The transaction costs for HAS (Hasbro), a typical DRIP stock, were discussed in the previous post. Hasbro’s fee schedule is reproduced below.

Example Fee Schedule

The fee structure for Hasbro (HAS) is:

DRIP vs Mutual Fund – Head to Head

In the following Excel spreadsheet you can see the effect of equal investment streams going into a DRIP account compared to a no-load mutual fund with zero brokerage commissions, a 1% annual management fee, 4% reinvested dividend yields, and 6% annual net asset value (NAV) growth. These are pretty decent numbers for a mutual fund. Few have done this well over any significant time period.

After 25 years the mutual fund’s value grows to $56,609.17. The same investment stream in a DRIP grows to $64,858.64 – a difference favorable to the DRIP of $8,249.47; A much larger difference than buying individual stocks thru a broker.

Why? Because the 1% management fee is 1% of the entire value of the investment – every year. Brokerage commissions are incurred only when you buy or sell. Frequent trading will cause commissions to mount up fast. But, if you hold high quality stocks for the long term commissions are insignificant.

What If?

This example is designed to be favorable to the mutual fund. Few mutual funds yield 4% dividends and few have management fees as low as 1%. Only index funds are that efficient and not all of them.

You can change the parameters in this spreadsheet.

Experiment with different commission fees, dividend yields, EPS growth rates or annual investments and see how they affect results. For example, changing the annual management fee to 0.5% reduces the difference to just $3,086.64 – still much more than when DRIPs are compared to buying and holding stock thru a broker.

The topic of the next post is Dollar-Cost Averaging.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Tuesday, October 12, 2010

How to Get Rich Slowly DRIP by DRIP: Transaction Costs Compared to Brokerages

You pay less for the privilege of DRIP account investing compared to using a broker – or mutual funds, but that’s another post.

Paying less to play means more money goes into your investment - increasing your net worth.

You buy stocks for your DRIP plan directly from the stock issuing company. The “Transfer Agent” merely administers the transactions. This means each DRIP plan can have a different fee structure. Some plans charge fees for purchases, some discount the purchase price from the current market price. All charge a fee when you sell.

Example Fee Schedule

The fee structure for Hasbro (HAS) is shown below.

Paying less to play means more money goes into your investment - increasing your net worth.

You buy stocks for your DRIP plan directly from the stock issuing company. The “Transfer Agent” merely administers the transactions. This means each DRIP plan can have a different fee structure. Some plans charge fees for purchases, some discount the purchase price from the current market price. All charge a fee when you sell.

Example Fee Schedule

The fee structure for Hasbro (HAS) is shown below.

HAS doesn’t allow buying the initial investment thru the plan administrator (Transfer Agent). You must transfer at least one share from your broker or mail an actual stock certificates to set up the account. As shown in the table above, there’s no fee to set up the account.

After the account is set up you can buy additional shares thru the Transfer Agent without fees. If you buy shares thru a broker you will pay a brokerage commission with each transaction. As a point of reference, my transaction costs thru my broker are $5.95 per transaction.

DRIP’s Aren’t for Trading

My broker charges the same $5.95 per transaction whether I’m buying or selling. You can see in the chart that Hasbro charges $10.00 per transaction PLUS $0.15 per share when you sell. So if I sold all of my HAS shares – assuming I owned 100 shares – my DRIP selling cost would be $10 + $15 (100 shares * $0.15/share) = $25 compared to only $5.95 if I sold the same 100 shares thru my broker. DRIP accounts are not for trading.

If you accumulate shares in your DRIP and hold them for the long term, the DRIP is very efficient in terms of transaction costs. None are charged on your monthly purchases. If I bought shares monthly thru my broker I’d pay $71.40 a year compared to zero in my DRIP. The higher DRIP selling fee is overwhelmed by the commissions charged on regular purchases of stock thru a broker.

DRIP vs Brokerage – Head to Head

In the Excel spreadsheet below you can see the effect of equal investment streams going into a DRIP account compared to a brokerage account given $5.95 brokerage commissions, 4% reinvested dividend yields, and 6% annual growth in earnings per share (EPS).

After 25 years the Brokerage investment stream grows to a value of $64,279.42. The same investment stream in a DRIP grows to $64,858.64 – a favorable difference to the DRIP of $579.22. Not much over 25 years.

What If?

This example, however, is designed to be extremely favorable to the brokerage account. There’s no trading and the buys are lumped into annual purchases of $600 each. In the DRIP, the annual $600 investment could be monthly purchases of $50 each – still with zero transaction costs. An equivalent investment stream in the brokerage account would reduce the value of the account to $57,197.38 – a favorable advantage to the DRIP of $6,950.58.

You can change the parameters in this spreadsheet.

Experiment with different commission fees, dividend yields, EPS growth rates or annual investments and see how they would affect results

In the next post, I’ll compare DRIP account investments to mutual funds. I think the results will surprise you.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

After the account is set up you can buy additional shares thru the Transfer Agent without fees. If you buy shares thru a broker you will pay a brokerage commission with each transaction. As a point of reference, my transaction costs thru my broker are $5.95 per transaction.

DRIP’s Aren’t for Trading

My broker charges the same $5.95 per transaction whether I’m buying or selling. You can see in the chart that Hasbro charges $10.00 per transaction PLUS $0.15 per share when you sell. So if I sold all of my HAS shares – assuming I owned 100 shares – my DRIP selling cost would be $10 + $15 (100 shares * $0.15/share) = $25 compared to only $5.95 if I sold the same 100 shares thru my broker. DRIP accounts are not for trading.

If you accumulate shares in your DRIP and hold them for the long term, the DRIP is very efficient in terms of transaction costs. None are charged on your monthly purchases. If I bought shares monthly thru my broker I’d pay $71.40 a year compared to zero in my DRIP. The higher DRIP selling fee is overwhelmed by the commissions charged on regular purchases of stock thru a broker.

DRIP vs Brokerage – Head to Head

In the Excel spreadsheet below you can see the effect of equal investment streams going into a DRIP account compared to a brokerage account given $5.95 brokerage commissions, 4% reinvested dividend yields, and 6% annual growth in earnings per share (EPS).

After 25 years the Brokerage investment stream grows to a value of $64,279.42. The same investment stream in a DRIP grows to $64,858.64 – a favorable difference to the DRIP of $579.22. Not much over 25 years.

What If?

This example, however, is designed to be extremely favorable to the brokerage account. There’s no trading and the buys are lumped into annual purchases of $600 each. In the DRIP, the annual $600 investment could be monthly purchases of $50 each – still with zero transaction costs. An equivalent investment stream in the brokerage account would reduce the value of the account to $57,197.38 – a favorable advantage to the DRIP of $6,950.58.

You can change the parameters in this spreadsheet.

Experiment with different commission fees, dividend yields, EPS growth rates or annual investments and see how they would affect results

In the next post, I’ll compare DRIP account investments to mutual funds. I think the results will surprise you.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Wednesday, October 6, 2010

How to Get Rich Slowly DRIP by DRIP: How to Reinvest Your Dividends

Adding the power of compounding dividends, regular dividend increases and appreciating share value will produce a much higher investment value over many years. I strongly recommend you reinvest your dividends – at least until you need them for income.

The Computershare web site isn’t the friendliest. But setting up your Computershare DRIP account to automatically reinvest dividends is easy despite awkward site navigation.

The embedded slide presentation contains instructions to will help you avoid minor inconveniences I’ve run into on http://www.computershare.com/.

Transaction costs are the subject of the next post.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

The Computershare web site isn’t the friendliest. But setting up your Computershare DRIP account to automatically reinvest dividends is easy despite awkward site navigation.

The embedded slide presentation contains instructions to will help you avoid minor inconveniences I’ve run into on http://www.computershare.com/.

Transaction costs are the subject of the next post.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Friday, October 1, 2010

How to Get Rich Slowly DRIP by DRIP: Why Should You Reinvest Your Dividends?

Well, why SHOULD you reinvest your dividends?

You could take your dividend money in cash and spend it. And, one day you will want to do just that. I plan to use future dividends as a major source of retirement income.

But until then, my dividends are reinvested.

Dividend Growth Stock

A well chosen dividend growth stock has demonstrated its ability to grow earnings per share and therefore - over time – its share value. It’s also increased its annual dividend in proportion to earnings growth.

A company may not do in the future what it did in the past; it’s nevertheless more likely to continue such policies than is a company that’s never consistently grown its earnings and dividends.

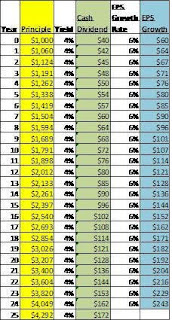

Compounding Earnings per Share (EPS)

A conservative example of a typical dividend growth stock – perhaps an electric utility – is shown in the chart below.

An original investment valued at $1,000 is assumed; with no additional future purchases. All dividends are assumed paid in cash and used as disposable income.

For simplicity, the normal fluctuations of business are assumed away - at conservative averages. A constant 4% dividend yield is assumed; as is constant annual earnings per share (EPS) growth of 6%. Constant market valuation based on the Price/Earnings Ratio (P/E) would make the value of the investment increase at the same 6% rate of EPS growth. Also, all compounding is shown as annual. Quarterly compounding (the reality) would increase the resulting values in all cases.

After 25 years of 6% annual growth your original $1,000 investment is worth $4,292 and the you received $2,366 in quarterly dividend payouts. Not bad.

Compounding EPS & Dividends

The next chart uses the same assumptions except instead of spending the dividends; you automatically reinvests them in additional shares of the company’s stock.

Look at what happens to your investment value. Look at what happens to your annual dividends available for retirement income at the end of year 25.

The $1,000 investment has grown to $10,835 and your annual disposable dividend income is $433 – more than twice as much and a nice chunk of change. Congratulations!

Compounding With Monthly Investments

Now what would become of your original $1,000 if you also made additional $25 monthly investments or $300 per year?

After 25 years of adding $25 per month to your investment – a total of $7,500 – your $8,500 (original $1,000 + the additional $7,500) is now worth $40,339. And, your available dividend income is $14,349 per year. Wow!

Getting Rich DRIP by DRIP

Suppose you did that with two or three more stocks – or even five. Suppose you increased your monthly investments as your income grows – say 3% per year.

In the chart above you start out with five $1,000 investments and add $25 per month to each of them. You increase your monthly investments by 3% per year and end up with a total cash investment of $15,938 ($5,000 original investment + $10, 938 in total monthly investments over 25 years).

This produces a value of $91,635. Your dividend income rises to $33,944 a year; all with a very modest commitment.

You can do even better that that – you can get rich DRIP by DRIP.

In the next post I’ll show you how to set up your DRIP account to automatically reinvest your dividends. It’s easy. It’s worth it.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

You could take your dividend money in cash and spend it. And, one day you will want to do just that. I plan to use future dividends as a major source of retirement income.

But until then, my dividends are reinvested.

Dividend Growth Stock

A well chosen dividend growth stock has demonstrated its ability to grow earnings per share and therefore - over time – its share value. It’s also increased its annual dividend in proportion to earnings growth.

A company may not do in the future what it did in the past; it’s nevertheless more likely to continue such policies than is a company that’s never consistently grown its earnings and dividends.

Compounding Earnings per Share (EPS)

A conservative example of a typical dividend growth stock – perhaps an electric utility – is shown in the chart below.

An original investment valued at $1,000 is assumed; with no additional future purchases. All dividends are assumed paid in cash and used as disposable income.

For simplicity, the normal fluctuations of business are assumed away - at conservative averages. A constant 4% dividend yield is assumed; as is constant annual earnings per share (EPS) growth of 6%. Constant market valuation based on the Price/Earnings Ratio (P/E) would make the value of the investment increase at the same 6% rate of EPS growth. Also, all compounding is shown as annual. Quarterly compounding (the reality) would increase the resulting values in all cases.

After 25 years of 6% annual growth your original $1,000 investment is worth $4,292 and the you received $2,366 in quarterly dividend payouts. Not bad.

Compounding EPS & Dividends

The next chart uses the same assumptions except instead of spending the dividends; you automatically reinvests them in additional shares of the company’s stock.

Look at what happens to your investment value. Look at what happens to your annual dividends available for retirement income at the end of year 25.

The $1,000 investment has grown to $10,835 and your annual disposable dividend income is $433 – more than twice as much and a nice chunk of change. Congratulations!

Compounding With Monthly Investments

Now what would become of your original $1,000 if you also made additional $25 monthly investments or $300 per year?

After 25 years of adding $25 per month to your investment – a total of $7,500 – your $8,500 (original $1,000 + the additional $7,500) is now worth $40,339. And, your available dividend income is $14,349 per year. Wow!

Getting Rich DRIP by DRIP

Suppose you did that with two or three more stocks – or even five. Suppose you increased your monthly investments as your income grows – say 3% per year.

In the chart above you start out with five $1,000 investments and add $25 per month to each of them. You increase your monthly investments by 3% per year and end up with a total cash investment of $15,938 ($5,000 original investment + $10, 938 in total monthly investments over 25 years).

This produces a value of $91,635. Your dividend income rises to $33,944 a year; all with a very modest commitment.

You can do even better that that – you can get rich DRIP by DRIP.

In the next post I’ll show you how to set up your DRIP account to automatically reinvest your dividends. It’s easy. It’s worth it.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, September 23, 2010

How to Get Rich Slowly DRIP by DRIP: More Follow Up Investments

Do you want to be “an investor” but don’t have the cash? Are you saving for retirement or a trip around the world – but you can’t see how you’ll reach your goal?

A Dividend ReInvestment Plan account (DRIP) – might be the solution.

The Main Thing

The main thing you need to know about DRIP accounts is you can start one for $250.00 or less and make follow up investments as low as $10 to $100.

Follow Up Investment Frequency

After you establish a DRIP you can, if you choose, add money every month or whenever you want – including never again.

When I contribute money to my DRIP it’s held until the next monthly purchase. Computershare, my DRIP administrator, seems to execute purchases between the 18th and the 22nd of the month – regardless of when you send in the money. If you miss their window they just queue it up for the regular purchase time – next month.

Follow Up Investment Fees

Most companies don’t charge fees or commissions to make follow up purchases. They generally do charge fees if you make your initial purchase thru the DRIP administrator instead of transferring shares from a broker. Remember you are buying stock from the issuing company, not from the DRIP administrator.

Example

A Dividend ReInvestment Plan account (DRIP) – might be the solution.

The Main Thing

The main thing you need to know about DRIP accounts is you can start one for $250.00 or less and make follow up investments as low as $10 to $100.

Follow Up Investment Frequency

After you establish a DRIP you can, if you choose, add money every month or whenever you want – including never again.

When I contribute money to my DRIP it’s held until the next monthly purchase. Computershare, my DRIP administrator, seems to execute purchases between the 18th and the 22nd of the month – regardless of when you send in the money. If you miss their window they just queue it up for the regular purchase time – next month.

Follow Up Investment Fees

Most companies don’t charge fees or commissions to make follow up purchases. They generally do charge fees if you make your initial purchase thru the DRIP administrator instead of transferring shares from a broker. Remember you are buying stock from the issuing company, not from the DRIP administrator.

Example

I contributed $25 via a checking account draft that is set up to occur every month. On 9/15/2010, Computershare bought from Hasbro 0.567924 shares of HAS common stock at a market price of $44.020000 per share. On 9/20/2010 the 0.567924 shares of HAS were credited to my DRIP account.

The exact same thing happens when I send money to a DRIP without the benefit of a regular monthly bank draft. I set up a one-time draft in those cases.

Although writing paper checks is an available option I don’t use that method. I just don’t trust that checks will always get where they’re supposed to go in a timely manner.

Results

In my Hasbro DRIP account I buy $25 worth of HAS stock every month. Because the price varies with the market, I buy a different amount of stock each time.

The table above shows the monthly purchases of HAS I’ve made starting with my November 2009 purchase. In every case, I bought $25 worth of HAS. You can see that every month I bought a smaller fractional share beginning with 0.849615 shares and ending with my most recent purchase of 0.567924.

The table above shows the monthly purchases of HAS I’ve made starting with my November 2009 purchase. In every case, I bought $25 worth of HAS. You can see that every month I bought a smaller fractional share beginning with 0.849615 shares and ending with my most recent purchase of 0.567924.This is a “good news/bad news” situation. I’m buying fewer shares for my $25 because the share price is going up – significantly. Because the stock price is going up, the value of my account is going up too. However, my monthly $25 buys fewer shares.

This Is Real

This really works. I set up my HAS account by transferring shares from my broker. I could’ve bought a single share thru my broker. If I did, my cost structure would’ve looked like this.

In October 2009, the market value of one share of HAS was $29.42. If I’d just opened the brokerage account and didn’t qualify for any commission discounts, the commission on a one share purchase would have been $19.95; so, $49.37 would’ve been my initial startup cost.

$29.42 + $19.95 = $49.37.

I didn’t buy just one share and the commission I paid was lower. The startup cost is hypothetical. But, the chart below shows the reality of my recent experience adjusted for the initial purchase of one share at a maximum commission rate. This is a real life example of what can happen with a DRIP.

Hasbro has did very well in the twelve months shown. My Hasbro DRIP has been open for two years and it’s done even better. Not every stock will do as well. Hasbro may never do as well again. But a DRIP can put you in the stock market at a very low cost.

Hasbro has did very well in the twelve months shown. My Hasbro DRIP has been open for two years and it’s done even better. Not every stock will do as well. Hasbro may never do as well again. But a DRIP can put you in the stock market at a very low cost.Remember that DRIP means Dividend ReInvestment Plan. I haven’t yet mentioned dividends. That’s for next time.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, September 16, 2010

How to Get Rich Slowly DRIP by DRIP: Follow Up Investments

Do you want to be “an investor” but you don’t have the cash? Do you want to save for retirement or a trip around the world – but you can’t see how you’ll reach your goal?

If you answered “yes”, a DRIP account – a Dividend ReInvestment Plan account – might be the solution.

The Main Thing

Here’s the main thing you need to know about DRIP accounts – you can start one for $250.00 or less with minimum follow up investments of between $10 & $100.

After you establish the account you can, if you choose, add money once a month.

Automatic Monthly Investments

Computershare, the DRIP account administrator for my accounts, offers an automatic bank draft for your regular monthly investments. I use this feature for two of my three accounts, HAS (Hasbro) & CTL (CenturyLink). Both companies require minimum follow up investments of $25 - I investment the minimum each month.

Infrequent At Will Investments

In my third DRIP account, SJM (JM Smucker), I occasionally make a follow up investment. Follow up’s can’t be more frequent than once a month – I add money far less often.

Bank Drafts vs. Mail-In Checks

You can still use the bank draft system even if you aren’t making regular monthly investments. Or, you can mail-in paper checks with the convenient “deposit” form provided by Computershare with the monthly account statement.

More - follow up investment information - to come in the next post.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

If you answered “yes”, a DRIP account – a Dividend ReInvestment Plan account – might be the solution.

The Main Thing

Here’s the main thing you need to know about DRIP accounts – you can start one for $250.00 or less with minimum follow up investments of between $10 & $100.

After you establish the account you can, if you choose, add money once a month.

Automatic Monthly Investments

Computershare, the DRIP account administrator for my accounts, offers an automatic bank draft for your regular monthly investments. I use this feature for two of my three accounts, HAS (Hasbro) & CTL (CenturyLink). Both companies require minimum follow up investments of $25 - I investment the minimum each month.

Infrequent At Will Investments

In my third DRIP account, SJM (JM Smucker), I occasionally make a follow up investment. Follow up’s can’t be more frequent than once a month – I add money far less often.

Bank Drafts vs. Mail-In Checks

You can still use the bank draft system even if you aren’t making regular monthly investments. Or, you can mail-in paper checks with the convenient “deposit” form provided by Computershare with the monthly account statement.

More - follow up investment information - to come in the next post.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Monday, September 13, 2010

How to Get Rich Slowly DRIP by DRIP

Links to Topics in the Special Report: How to Get Rich Slowly DRIP by DRIP

DRIP by DRIP: Introduction

DRIP by DRIP: The Initial Investment

DRIP by DRIP: Follow Up Investments

DRIP By DRIP: More Follow Up Investments

DRIP by DRIP: Why Should You Reinvest Your Dividends?

DRIP by DRIP: How to Reinvest Your Dividends

DRIP by DRIP: Transaction Costs Compared to Brokerages

DRIP by DRIP: Transaction Costs Compared to Mutual Funds

DRIP by DRIP: What's Dollar-Cost Averaging Got to do with It?

DRIP by DRIP: Diversification in a DRIP

DRIP by DRIP: Asset Allocation

DRIP by DRIP: Gifts to Children

DRIP by DRIP: Gifts to My Children

DRIP by DRIP: Set Up for Dividend Reinvestment

DRIP by DRIP: Set Up a One-Time Investment

DRIP by DRIP: Transaction History

Link to the Special Report: Dividends

Dividends - Part 1 - Introduction

DRIP by DRIP: Introduction

DRIP by DRIP: The Initial Investment

DRIP by DRIP: Follow Up Investments

DRIP By DRIP: More Follow Up Investments

DRIP by DRIP: Why Should You Reinvest Your Dividends?

DRIP by DRIP: How to Reinvest Your Dividends

DRIP by DRIP: Transaction Costs Compared to Brokerages

DRIP by DRIP: Transaction Costs Compared to Mutual Funds

DRIP by DRIP: What's Dollar-Cost Averaging Got to do with It?

DRIP by DRIP: Diversification in a DRIP

DRIP by DRIP: Asset Allocation

DRIP by DRIP: Gifts to Children

DRIP by DRIP: Gifts to My Children

DRIP by DRIP: Set Up for Dividend Reinvestment

DRIP by DRIP: Set Up a One-Time Investment

DRIP by DRIP: Transaction History

Link to the Special Report: Dividends

Dividends - Part 1 - Introduction

Thursday, September 9, 2010

How to Get Rich Slowly DRIP by DRIP: The Initial Investment

Do you want to be “an investor” but you don’t have the cash? Do you want to save for retirement or a trip around the world – but you can’t see how you’ll reach your goal?

If you answered “yes”, a DRIP account – a Dividend ReInvestment Plan account – might be the solution.

The Main Thing

There’s a lot to learn about DRIP accounts. I’ll go there later. But here is the main thing you need to know – you can start one for $250.00 or less with follow up investments in some cases as low as $10 per purchase.

In my DRIP account I currently have three stocks, Hasbro Corp (HAS), CenturyLink (CTL), and JM Smucker (SJM).

Transferring Stock

When I opened the HAS account I bought shares through an on-line brokerage house and transferred one share from the brokerage to the DRIP plan administrator, Computershare.

As I write this, HAS closed the trading day at a price of $43.05 & CLT closed at $36.47. On-line brokerage houses have different commission schedules ranging from as low as $4.00 per trade to as high as $20.00 per trade. Worst case – you could today open a Hasbro DRIP for $63.05 ($43.05 stock price + $20.00 commission) and a CenturyLink DRIP for $56.47 ($36.47 stock price + $20.00 commission).

Transferring the stock from the brokerage to Computershare must be done by the brokerage house. In my case, I wrote a letter to my brokerage, USAA Brokerage Services, instructing them to send one share of HAS to Computershare. In the letter I provided my brokerage account number, my home address, the number of shares to transfer, and the address and phone number of Computershare.

After about a week the transaction was complete. One share of HAS appeared in my new DRIP account at Computershare.

One thing surprised me the first time thru this process. Computershare did ALL of the account set up after receiving the stock certificate from USAA. They wouldn’t do any preliminary set up although I asked them to.

Direct Buy

When I set up the account for JM Smucker (SJM) I made the initial purchase thru Computershare. Some companies that offer their shares thru DRIP account administrators allow direct purchase of the initial investment - but many don’t. For those that don’t you must set up the account by transferring at least one share as described above.

For SJM though, I set up a purchase using the Computershare web site for the minimum allowed initial investment of $250.00. When the transaction was processed (they process buy orders once a month) the price of SJM was $54.904952 and they charged a transaction fee of $11.93. This netted me 4.336039 shares of SJM.

Yes, they sell fractional shares & yes, they priced the shares to six decimal places.

The actual fee schedules are complicated and they’re different for every company. You’re actually buying shares of the company from the company. In my case I bought 4.336039 shares of JM Smucker (SJM) directly from JM Smucker. Computershare merely facilitated the transaction and now holds the shares on my behalf.

Because you buy directly from the share-issuing company, each company sets their own rules for how the transaction is handled and how much it costs.

In my next post I’ll review follow up investments. In the cases of HAS, CTL, and SJM the minimum follow up investment is $25.00.

The Main Thing

At Computershare the minimum follow up ranges from $10.00 to $100.00 per transaction. But you can already see that a Hasbro DRIP account can be started for $60 to $70 or less (depending on the current price per share & your specific brokerage commission). And, follow up investments in HAS can be as little as $25.00.

Get Rich Slowly

$25 per month doesn’t sound like much, but over 30 or more years of stock price appreciation combined with compounded reinvested dividends – you can get rich slowly.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

If you answered “yes”, a DRIP account – a Dividend ReInvestment Plan account – might be the solution.

The Main Thing

There’s a lot to learn about DRIP accounts. I’ll go there later. But here is the main thing you need to know – you can start one for $250.00 or less with follow up investments in some cases as low as $10 per purchase.

In my DRIP account I currently have three stocks, Hasbro Corp (HAS), CenturyLink (CTL), and JM Smucker (SJM).

Transferring Stock

When I opened the HAS account I bought shares through an on-line brokerage house and transferred one share from the brokerage to the DRIP plan administrator, Computershare.

As I write this, HAS closed the trading day at a price of $43.05 & CLT closed at $36.47. On-line brokerage houses have different commission schedules ranging from as low as $4.00 per trade to as high as $20.00 per trade. Worst case – you could today open a Hasbro DRIP for $63.05 ($43.05 stock price + $20.00 commission) and a CenturyLink DRIP for $56.47 ($36.47 stock price + $20.00 commission).

Transferring the stock from the brokerage to Computershare must be done by the brokerage house. In my case, I wrote a letter to my brokerage, USAA Brokerage Services, instructing them to send one share of HAS to Computershare. In the letter I provided my brokerage account number, my home address, the number of shares to transfer, and the address and phone number of Computershare.

After about a week the transaction was complete. One share of HAS appeared in my new DRIP account at Computershare.

One thing surprised me the first time thru this process. Computershare did ALL of the account set up after receiving the stock certificate from USAA. They wouldn’t do any preliminary set up although I asked them to.

Direct Buy

When I set up the account for JM Smucker (SJM) I made the initial purchase thru Computershare. Some companies that offer their shares thru DRIP account administrators allow direct purchase of the initial investment - but many don’t. For those that don’t you must set up the account by transferring at least one share as described above.

For SJM though, I set up a purchase using the Computershare web site for the minimum allowed initial investment of $250.00. When the transaction was processed (they process buy orders once a month) the price of SJM was $54.904952 and they charged a transaction fee of $11.93. This netted me 4.336039 shares of SJM.

Yes, they sell fractional shares & yes, they priced the shares to six decimal places.

The actual fee schedules are complicated and they’re different for every company. You’re actually buying shares of the company from the company. In my case I bought 4.336039 shares of JM Smucker (SJM) directly from JM Smucker. Computershare merely facilitated the transaction and now holds the shares on my behalf.

Because you buy directly from the share-issuing company, each company sets their own rules for how the transaction is handled and how much it costs.

In my next post I’ll review follow up investments. In the cases of HAS, CTL, and SJM the minimum follow up investment is $25.00.

The Main Thing

At Computershare the minimum follow up ranges from $10.00 to $100.00 per transaction. But you can already see that a Hasbro DRIP account can be started for $60 to $70 or less (depending on the current price per share & your specific brokerage commission). And, follow up investments in HAS can be as little as $25.00.

Get Rich Slowly

$25 per month doesn’t sound like much, but over 30 or more years of stock price appreciation combined with compounded reinvested dividends – you can get rich slowly.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Thursday, September 2, 2010

How to Get Rich Slowly DRIP by DRIP: Introduction

Would you like to be “an investor” but you just don’t have the cash? Are you trying to save money for retirement, for a dream home, for a child’s education, for a trip around the world – but you can’t see how the little bit you’re saving each month will ever allow you to reach your goal?

If you answered “yes” to any part of these questions, a DRIP account – a Dividend ReInvestment Account –may be just what you need.

In the series to follow, I’ll discuss DRIP accounts in detail. I hope some of you will decide, as I did, that DRIP accounts are wonderful things; that they deserve a place in your financial plan.

I’ll point out the advantages & disadvantages of investing thru DRIP’s and I’ll provide instructions on how you can set one up.

Below are the main DRIP account topics I’ll explore:

· Inexpensive – zero or very low transaction costs

· Automatic Dividend re-investment

· Low initial investment

· Low minimum follow up investments

· Automatic monthly investments – debit checking or savings account

· Dollar-Cost Averaging

· Compounding

· Gift to children – minor or adult

· Difficult to set up

· Easy to administer after initial set up

· Limited investment choices

· Difficult to move between investments

· Manage thru allocation of new money

· Step by Step thru the set up process

· Step by Step thru the monthly purchase process

· DRIP Plan Administrators

· DRIP Plan Investment Choices

· DRIP vs DSPP

I urge you to follow along as I present the attributes of Dividend ReInvestment Accounts. I believe this investment vehicle deserves far more attention that it gets. It’s truly a way to “Get Rich Slowly”.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Link to the Special Report: "Dividends"

If you answered “yes” to any part of these questions, a DRIP account – a Dividend ReInvestment Account –may be just what you need.

In the series to follow, I’ll discuss DRIP accounts in detail. I hope some of you will decide, as I did, that DRIP accounts are wonderful things; that they deserve a place in your financial plan.

I’ll point out the advantages & disadvantages of investing thru DRIP’s and I’ll provide instructions on how you can set one up.

Below are the main DRIP account topics I’ll explore:

· Inexpensive – zero or very low transaction costs

· Automatic Dividend re-investment

· Low initial investment

· Low minimum follow up investments

· Automatic monthly investments – debit checking or savings account

· Dollar-Cost Averaging

· Compounding

· Gift to children – minor or adult

· Difficult to set up

· Easy to administer after initial set up

· Limited investment choices

· Difficult to move between investments

· Manage thru allocation of new money

· Step by Step thru the set up process

· Step by Step thru the monthly purchase process

· DRIP Plan Administrators

· DRIP Plan Investment Choices

· DRIP vs DSPP

I urge you to follow along as I present the attributes of Dividend ReInvestment Accounts. I believe this investment vehicle deserves far more attention that it gets. It’s truly a way to “Get Rich Slowly”.

Link to Topics in the Special Report - How to Get Rich Slowly DRIP by DRIP

Link to the Special Report: "Dividends"

Thursday, August 26, 2010

When to Sell: Reasons to Sell that are Unrelated to the Stock

When should I sell stock I bought as an investment?

At heart, I’m a “dividend growth” investor. So, logically, when a stock ceases to be a dividend growth stock I should sell it. But, economic cycles and temporary misfortunes don’t necessarily turn a good company bad. So, under what conditions should I decide that a formerly good dividend growth stock has ceased to be one?

In my previous two posts I identified four analytical criteria and three qualitative reasons I’ll use to make that decision. But there are other reasons I‘ll consider selling that are unrelated to a specific stock.

H. I’ll sell when I believe there is a market crash or a significant correction pending and I want to preserve my capital for reinvestment at substantially lower prices.

This happened in 2008. Although I was slow to recognize the crash, I did manage to sell everything I wanted to sell about 30% into the downward leg. I started buying again near the bottom and continued buying until the Dow approached 11,000. This enabled me in 2009 and 2010 to more than make up for my 2008 losses.

I believe we are on the verge of repeating the crash. Consequently, over the past weeks I’ve sold most of my equity positions so I’ll be prepared to start buying again when the market is 20% to 30% lower.

I don’t know how to time the market better than anyone else. But I’m convinced that the current economic “recovery” is phony and more importantly – it’s over. I’ve no idea where the bottom will be. That’s why I’ll start buying when the market is 20% to 30% down and I’ll continue buying a little at a time while events play out.

I hope to “dollar cost average” the market bottom and “bracket it” in field artillery terms.

I. I’ll sell my weakest investments when I need cash to invest in a much better opportunity.

When I identify a strong new investment opportunity and I have insufficient cash available to purchase it, I’ll chose one or more of my least attractive current positions to sell. Using the proceeds of the sale, I’ll buy the new stock.

In practice, I’m never fully invested. I maintain a cash reserve in case an extraordinary opportunity presents itself. However, if my reserve is at my minimum target value, I’ll still sell my weakest investments to raise additional cash for the new stock.

Since the recent rally peaked, I’ve steadily increased my cash reserve in preparation for the expected downturn. As my target cash reserve figure increased, there have been multiple occasions when I sold weaker investments to purchase stronger ones.

J. I’ll sell my weakest investments if an emergency situation requires more cash than I have available.

If a family disaster occurs selling investments could become necessary. However, my wife & I maintain emergency accounts as well as insurance that we hope will prevent this situation.

Retirement Income

Most people would include generating income in retirement as a reason to sell stocks; not me. I buy only dividend stocks and I plan to use only the dividends as retirement income. I’ll let the stocks appreciate over time and continue increasing their annual dividend payouts.

Summary of the Reasons I Will Sell Stocks

A. The company stops paying a dividend.

B. The stock’s price increases such that the dividend yield falls below 2% and the P/E ratio rises above 25.

C. The company’s earnings decline enough that the dividend payout ratio exceeds 100%.

D. The stock’s “Financial Score” is a negative number.

E. The company’s survival is threatened by a very large legal liability.

F. The company enters into a major merger agreement.

G. The stock’s total return falls below 10%.

H. I’ll sell when I believe there is a market crash or a significant correction pending and I want to preserve my capital for reinvestment at substantially lower prices.

I. I’ll sell my weakest investments when I need cash to invest in a much better opportunity.

J. I’ll sell my weakest investments if an emergency situation requires more cash than I have available.

I hope you find this series of posts on “When to Sell” interesting. Writing it has clarified my thinking about selling stock. For me, it was a profitable exercise.

Link to Topics in the Special Report: "When to Sell"

At heart, I’m a “dividend growth” investor. So, logically, when a stock ceases to be a dividend growth stock I should sell it. But, economic cycles and temporary misfortunes don’t necessarily turn a good company bad. So, under what conditions should I decide that a formerly good dividend growth stock has ceased to be one?

In my previous two posts I identified four analytical criteria and three qualitative reasons I’ll use to make that decision. But there are other reasons I‘ll consider selling that are unrelated to a specific stock.

H. I’ll sell when I believe there is a market crash or a significant correction pending and I want to preserve my capital for reinvestment at substantially lower prices.

This happened in 2008. Although I was slow to recognize the crash, I did manage to sell everything I wanted to sell about 30% into the downward leg. I started buying again near the bottom and continued buying until the Dow approached 11,000. This enabled me in 2009 and 2010 to more than make up for my 2008 losses.

I believe we are on the verge of repeating the crash. Consequently, over the past weeks I’ve sold most of my equity positions so I’ll be prepared to start buying again when the market is 20% to 30% lower.

I don’t know how to time the market better than anyone else. But I’m convinced that the current economic “recovery” is phony and more importantly – it’s over. I’ve no idea where the bottom will be. That’s why I’ll start buying when the market is 20% to 30% down and I’ll continue buying a little at a time while events play out.

I hope to “dollar cost average” the market bottom and “bracket it” in field artillery terms.

I. I’ll sell my weakest investments when I need cash to invest in a much better opportunity.

When I identify a strong new investment opportunity and I have insufficient cash available to purchase it, I’ll chose one or more of my least attractive current positions to sell. Using the proceeds of the sale, I’ll buy the new stock.

In practice, I’m never fully invested. I maintain a cash reserve in case an extraordinary opportunity presents itself. However, if my reserve is at my minimum target value, I’ll still sell my weakest investments to raise additional cash for the new stock.

Since the recent rally peaked, I’ve steadily increased my cash reserve in preparation for the expected downturn. As my target cash reserve figure increased, there have been multiple occasions when I sold weaker investments to purchase stronger ones.

J. I’ll sell my weakest investments if an emergency situation requires more cash than I have available.